Imagine spending all your life working in order to build a business and accumulate wealth that should, by right, establish your legacy and family name. Yet, by the time your grandchildren come of age, the wealth that you worked so hard to establish has completely GONE! Sadly, this is the reality that is faced by more than 90% of all families globally! The saying ‘shirtsleeves to shirtsleeves within three generations’ is actually a fact that is faced by families

today. What is more worrying is that the amount of money is irrelevant. Cornelius Vanderbilt is a classic example of this. When he passed away in 1877, aged 82, he left a fortune of $215 billion (2016 dollars, inflation adjusted)1. Despite this huge fortune, it took only 70 years for the first bankruptcy to be declared within the family and in 1973 when the Vanderbilt had a family reunion there was not a single millionaire among them.

“It has left me with nothing to hope for, with nothing definite to seek or strive for. Inherited wealth is a real handicap to happiness. It is a certain death to ambition as cocaine is to morality.” William K Vanderbilt, grandson of the self-made Cornelius.

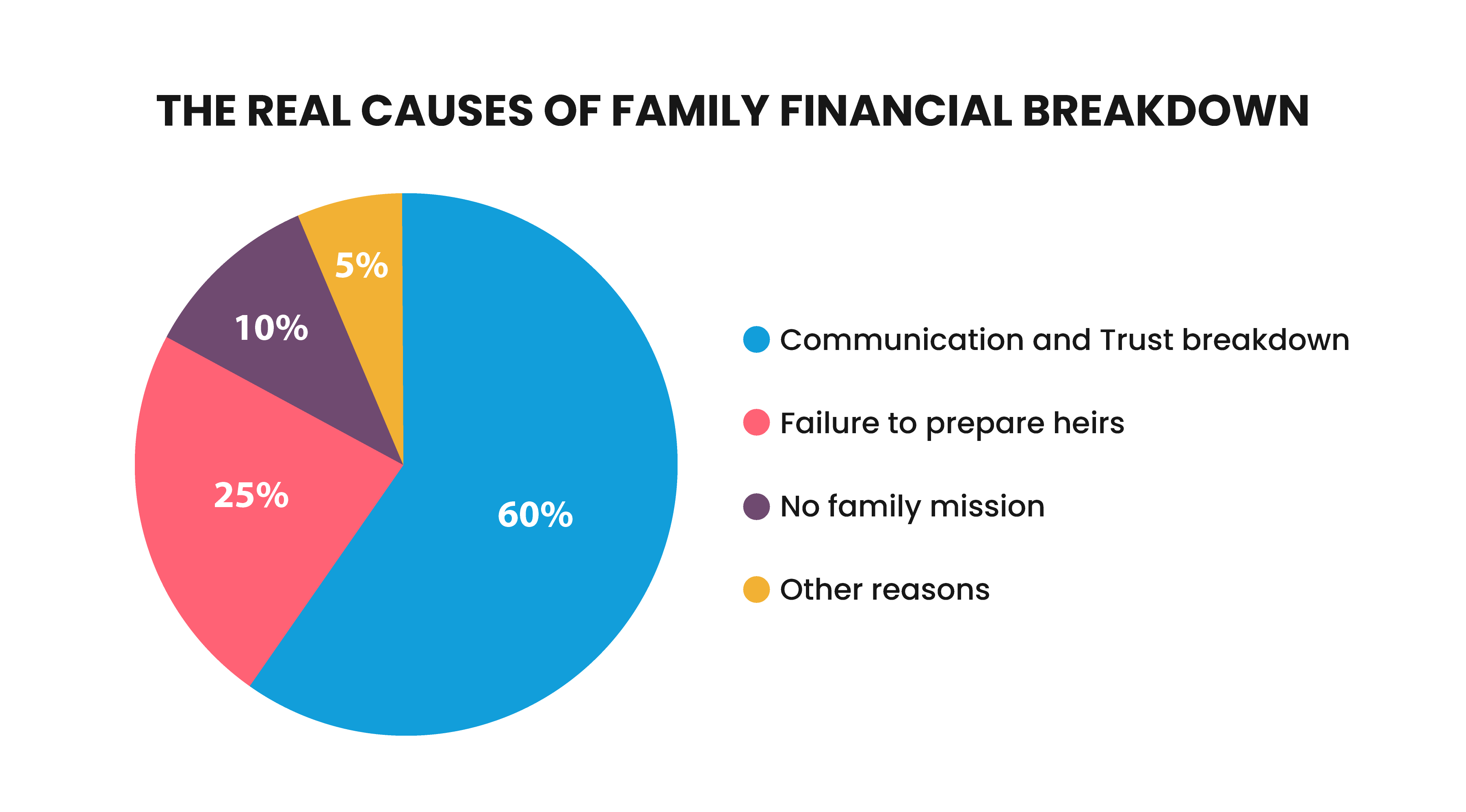

HOW MONEY FLOWS WITHIN THE FAMILY

Historical studies have proven that 70% of families will lose all their wealth within just two generations and more than 90% will lose it within three generations. This fact was further highlighted by the 2014 Forbes billionaire family list which revealed that out of the 483 families analysed, less than 10% were third generation! This distinct pattern can be highlighted as follows:

- First Generation (Create the Wealth) – The emphasis starts with learning how to create wealth, then shifts to creating and growing the wealth-generating business engine and dealing with cost

- Second Generation (Save the Wealth) – Of the 30% that successfully retain the wealth, this generation focuses on growing the business and further investing, so that hopefully, wealth creates further

- Third Generation (Spend the Wealth) – Wealth is received and spent by this generation, who do not hold a meaningful sense of responsibility for wealth management. In this generation, there is no appreciation for wealth or money, other than spending it.

The diagram below perfectly summarises this sad statistic.

The evidence is therefore clear, from history, from current research and in practice – 70% of families will lose all their wealth within two generations and over 90% will lose it within just three. So, what can families do and what actions must they take in order to avoid becoming another damning statistic? More importantly who within the family should be taking the responsibility to lead the family towards their desired collective vision?

The biggest mistake that any family can make is to believe that they are above the research and history. Underestimating the likelihood of a disaster and its possible effects is called Normality bias. This is a belief or mental state based on the false premise that things will always function the way things have normally functioned; but can one truly believe that just because everything is going well today then everything will be fine tomorrow?

How many companies have we seen in the past go bankrupt all because they believed in their own hype, failed to adapt to changing markets or simply thought they were too big to fail? Why should families believe they are any different?

Understanding the REAL Problem

It is essential for the family to firstly understand what the problem is, then to get clear on their ideal outcome before they seek to find a solution. Unfortunately, families are too quick to outsource what they think is the problem to professional advisors. Areas such as tax planning, estate planning and financial planning are valuable and should not be dismissed but they do not deal with the real underlying causes of multi-generational financial failure.

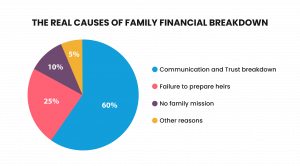

The Williams Group conducted the most detailed study in the area of family wealth and hi犀利士

ghlighted the real reasons why families lose all their wealth:

What is the most worrying aspect of this research is that even today very few families know or even appreciate what causes multi-generational failure. Only 5% of families lost their money because of poor tax, financial and legal planning yet the majority if not all professional advisors focus their expertise in these areas.

The message is therefore clear, effective family leadership is necessary to take pro-active measures to ensure the sustainability of the family dynamic. This is more than just about securing the financial wealth of the family, its about securing the family legacy by establishing healthy long-term relationships through effective communication and creating a purpose for the wealth that is greater than the individual wants of each family member. Successful, long standing families such as the Rockefellers and the Rothschilds have used their vast wealth to make significant impact on the world through their generous philanthropic ventures which can be measured in the billions of dollars. They have understood that a successful family, much like a successful business demands strong leadership and a clear purposeful vision that is shared by all family members. More importantly they appreciate that wealth is not simply measured in terms financial capital but also includes the human and intellectual capital – the story and knowhow behind the money. They ensure the multi-generational success of their family by passing all the wealth and not just the financial wealth and by doing so demonstrate strong effective leadership qualities that all families need to follow.

Statistics, research and history all suggest that families, irrespective of how much financial wealth they have are all fighting an uphill battle for survival. 70% of families will lose their wealth within just two generations whilst over 90% will lose it within just three generations. If one is serious about establishing a long-lasting family legacy and wants to avoid the implosion of their family relationship then strong, pro-active leadership is a must and not an option.

Prevention is better and significantly cheaper (both emotionally and financially) than a cure so why are families not taking the right action required? Maybe it is the inherent fear of communicating about the ‘elephant in the room’ such as openly communicating one’s estate to all family members? Maybe it is the arrogance that comes with having vast wealth? Maybe it’s the lack of understanding or even appreciating how big the problem truly is? Maybe its as simple as blindly trusting the existing advisors to keep the family and its assets together? The answer to this question is not obvious but the problem is very real.

As a family, if you do not know where you are (in terms of assessing the real risks to the family) and where you want to go, with a clear family vision, then how can you possibly expect to get the best suited advice? Professional advisors are bound by the instructions of their clients. They may be the best in their field of expertise, but they cannot be expected to understand or appreciate the family dynamic better than the family itself! To put this into perspective would anyone simply visit their doctor and ask to be fixed without even communicating the symptoms? Of course, not but why are families taking such unnecessary risks and simply ‘hoping for the best’? Therefore, only the families with strong leadership that encourage effective communication within the family, set out a vision that inspires all family members and create formal governance structures are the ones that not only survive but thrive over multiple generations.

“It requires a great deal of boldness and a great deal of caution to make a great fortune; and when you have got it, it requires 10 times more wit to keep it.” Nathan Rothschild

17 Apr, 2018

17 Apr, 2018

Nicholas Charles: my story, my why

Nicholas Charles, the founder of Charles Group, talks about his family history and the reasons why he feels Read more

28 Nov, 2019

28 Nov, 2019

What are the big myths around family prosperity?

Nicholas Charles, the founder of Charles Group, talks about his family history and the reasons why he feels Read more

4 Jun, 2018

4 Jun, 2018

The pains of the second generation of wealthy families (and why nobody understands them)

This is a story about a young man who came from a wonderful family, had a great upbringing, Read more

17 Aug, 2020

17 Aug, 2020

How Family Businesses Can Maintain Prosperity

Nicholas Charles, the founder of Charles Group, talks about his family history and the reasons why he feels Read more